Technology

Explained: Increased UPI payment charges; who will pay and what are the charges?

There has understandably been quite a flutter in the market, with news spreading of an interchange fee of up to 1.1% on UPI transactions done via Prepaid Payment Instruments (PPI) from April 1. However, there has been some confusion among consumers and merchants about who will be responsible for paying these fees.

While a statement was released to clarify this, a lot of it still left scope for confusion among consumers. We try to cut through the jargon and decode exactly what will happen from April 1 and how it will affect you.

UPI merchant transaction interchange fee- What does the NPCI say?

According to the National Payments Corporation of India (NPCI), which governs UPI, starting April 1, merchant transactions exceeding ₹2,000 in value done using Prepaid Payment Instruments (PPI Wallets) on UPI will attract an interchange charge of 1.1%. However, the new interchange charges are only applicable for the PPI merchant transactions and there is no charge to customers.

“The interchange charges introduced are only applicable for the PPI merchant transactions and there is no charge to customers, and it is further clarified that there are no charges for the bank account to bank account-based UPI payments (i.e., normal UPI payments),” NPCI said in a statement on Wednesday.

“It is further clarified that there are no charges for the bank account to bank account based UPI payments (i.e., normal UPI payments),” the NPCI added.

The Interchange fee is generally associated with card payments to cover transaction costs. In the statement, NCPI said as per recent regulatory guidelines, the PPI Wallets had been permitted to be part of the interoperable UPI ecosystem.

Rajsri Rengan, India Head of Development, Banking and Payments, at FIS said in a statement, “The new interoperability guidelines for prepaid payment instruments announced by the NPCI is a significant step towards building a more inclusive and seamless digital payments ecosystem in India.”

“The interoperability of digital wallets and UPI can be a game-changer for the Indian fintech industry, as it opens up new opportunities for innovation, growth, and competition. With greater interoperability between payment systems, consumers will have more choice and flexibility in how they transact with merchants, leading to increased adoption of digital payments and ultimately driving financial inclusion and economic growth”.

What is the interchange fee and who will have to pay?

Interchange fees are transaction fees that the merchant has to pay whenever a customer processes a transaction. So, if you are making a prepaid payment through UPI at a store using a PhonePe QR code, the merchant has to pay the interchange fee to the payment service provider, which is PhonePe in this example. Simply put, the interchange fee is similar to the merchant discount rate applicable to credit cards.

Which UPI payments will attract an interchange fee?

As stated by the NPCI, only certain merchant transactions made by prepaid payment instruments will attract the interchange fee. Wallets, smart cards, vouchers, magnetised chips come under prepaid payment instruments. A few examples of wallets are the Paytm wallet, PhonePe wallet, Amazon Pay, MobiKwik wallet, and SODEXO vouchers.

When a user makes a payment through these wallets to a merchant’s bank account, the merchant will be charged an interchange fee of 1.1%.

However, if you are a consumer using a digital wallet or prepaid payment instrument, you will not have to pay any fees.

It is important to note that these fees are not fixed and can vary from merchant to merchant. For specific industries, charges can range from 0.50% to 1.1% of the transaction value. Merchants are responsible for paying these charges, and they cannot be collected from customers.

How much are the interchange fees for UPI merchant transactions via PPI?

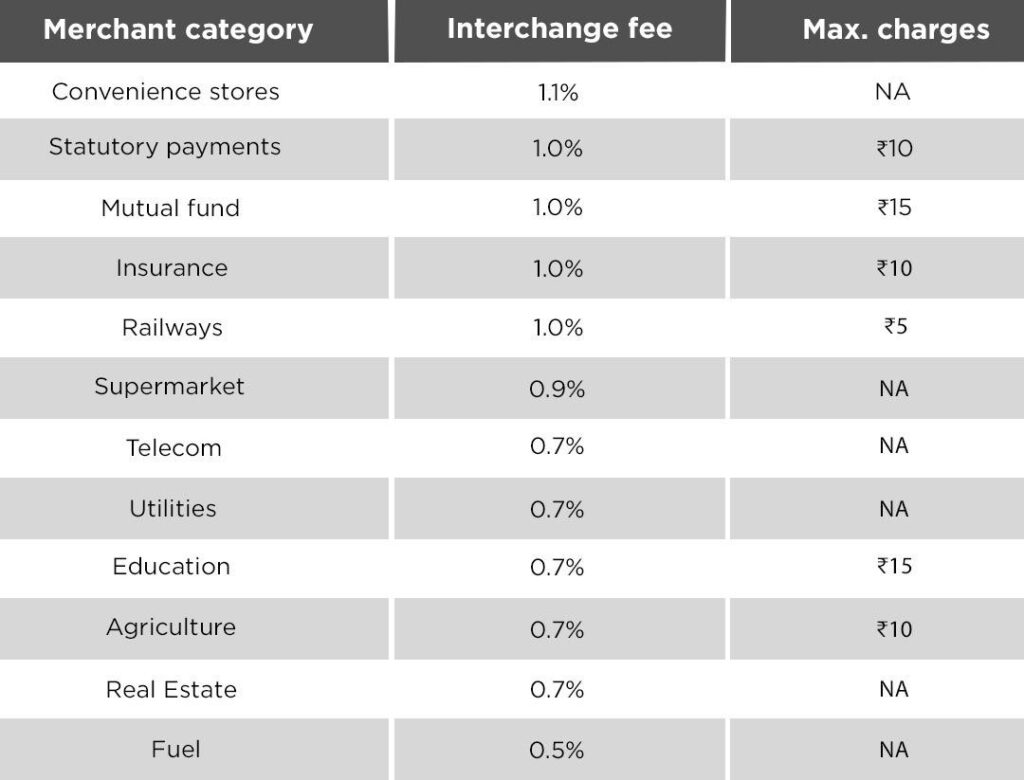

According to NPCI, the interchange fee will range from 0.5% to 1.1% depending on the merchant category codes. Payments for things like fuel, education, agriculture, and utilities will be subject to an interchange fee of 0.5%. There will be an interchange fee of 1.1% for establishments in categories such convenience stores and specialist retail outlets.

How much does it cost to send money to friends, family, or anyone else via UPI?

The interchange fee will not be applicable to Peer-to-Peer (P2P) transactions or Peer-to-Peer-Merchant (P2PM) transactions between a bank and the prepaid wallet, said NPCI. P2PM is the NPCI classification for small businesses which have a projected monthly inward UPI transaction of less than or equal to ₹50,000. So, if you are sending money to friends, family. or any other individual or a small business merchant’s bank account, it will not attract an interchange fee.

Is there a cost associated with reloading your Paytm, PhonePe, or Amazon Pay wallets?

In order to reload a wallet with more than ₹2,000, NPCI has mandated that PPI providers pay a wallet-loading service fee to the remitter bank of 15 basis points. For instance, Paytm will pay a wallet-loading service fee of 0.15% to your bank if you reload your Paytm, PhonePe, or Amazon Pay wallet with more than ₹2,000.

As of right now, there are no additional costs associated with recharging your wallet to do UPI transactions. However, if the wallet issuers decide to pass on the 15 basis points service fee, loading wallets could cost more.