Business

PhonePe: Value Creation and Appropriation in India’s Digital Payments Economy

Within the broader arc of Digital India, many platforms have achieved impressive scale. But scale, in isolation, is not a business model. The more consequential question is how a platform creates value for its users, merchants, and the wider financial ecosystem-and how effectively it appropriates a share of that value for itself.

That is precisely what makes PhonePe worth examining closely.

Since its launch in 2016, PhonePe has executed a deliberate journey from transactional utility to foundational financial infrastructure. It now sits at the intersection of payments, merchant services, financial products, and digital distribution-not merely riding India’s digital wave, but actively expanding the surface area from which it can both create and capture value.

As it approaches a public listing, the defining question is no longer how large PhonePe has grown. It is how durably it has built the mechanisms to sustain value creation and how structurally it has positioned itself to appropriate returns from that value over time.

1. Behavioral Embeddedness: The Foundation of Value Appropriation

Most consumer internet businesses define success through user acquisition. Downloads, registrations, sign-ups; these are treated as proxies for value creation.

But acquisition is merely the precondition. Durable value appropriation requires something harder to build: conversion into consistent, repeat behavior.

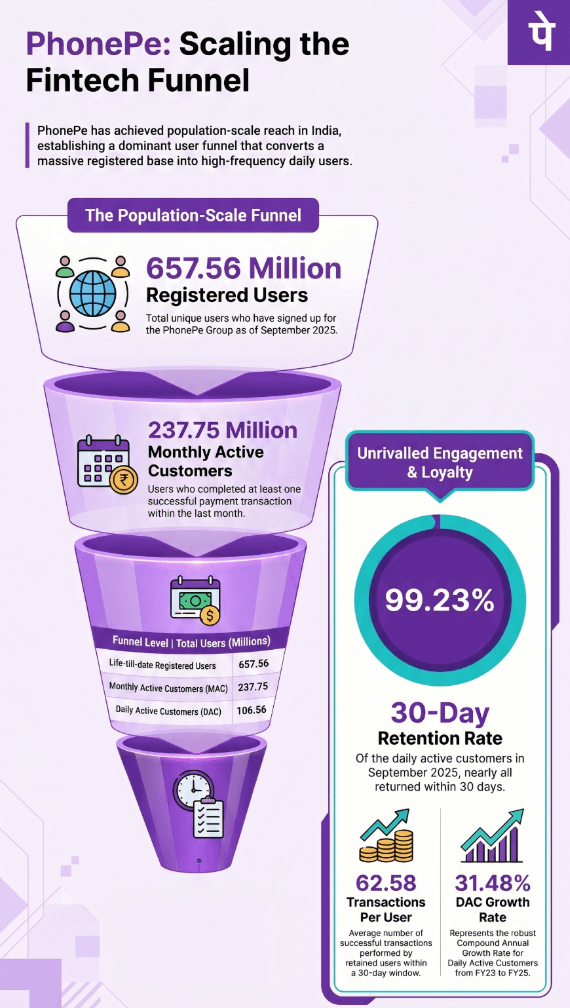

From app to instinct: India doesn’t just use PhonePe-it defaults to it

Source: PhonePe Draft Red Herring Prospectus filed with SEBI in Jan 2026

With over 657 million registered users, PhonePe operates at a population scale that few platforms anywhere in the world have reached. But the deeper value-creation story lies not in headcount, but in behavioral depth. A significant share of its base transacts regularly, reflecting a shift from occasional utility to habitual reliance.

High retention rates and rising daily engagement are symptoms of a more fundamental dynamic: behavioral lock-in. When a platform ceases to be something users choose and becomes something they instinctively reach for- switching costs rise sharply, and with them, the platform’s capacity to appropriate value from that relationship over the long term.

PhonePe has not merely grown its user base. It has embedded itself into a cognitive habit loop. That is a qualitatively different and far more defensible position.

2. Multi-Use-Case Dominance: Breadth as a Value Creation Multiplier

Market leadership in digital payments is often measured by aggregate transaction volumes. But those numbers can obscure a more important question: across which specific use-cases is that leadership earned?

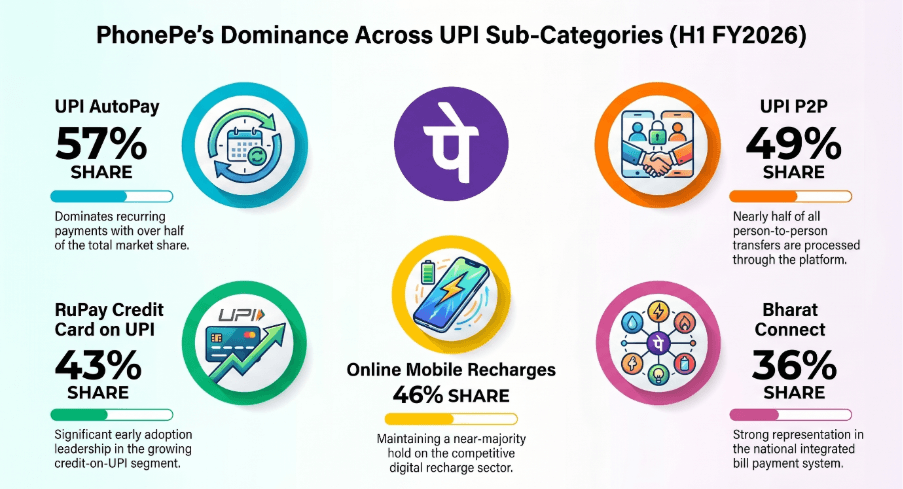

Category by category, PhonePe isn’t competing—it’s setting the benchmark

Source: PhonePe Draft Red Herring Prospectus filed with SEBI in Jan 2026

PhonePe’s value creation is not concentrated in a single vertical. It has built leadership across a wide range of high-frequency transaction categories-from recurring AutoPay mandates and peer-to-peer transfers to mobile recharges and emerging instruments like credit-on-UPI.

This breadth matters strategically for several reasons. First, it ensures that the platform is not exposed to disruption through a single use-case being displaced. Second, it transforms PhonePe from a one-purpose tool into a multi-utility financial interface-a default layer through which a diverse range of transactions flow.

And critically, the more use-cases a platform owns, the more data, engagement, and user trust it accumulates-each of which strengthens its capacity to appropriate value across adjacent services.

3. Proprietary Infrastructure: Value Creation Through Structural Cost Advantage

Behind every large-scale consumer platform lies an infrastructure layer that is either owned or rented. That choice carries profound implications for long-run value creation and appropriation.

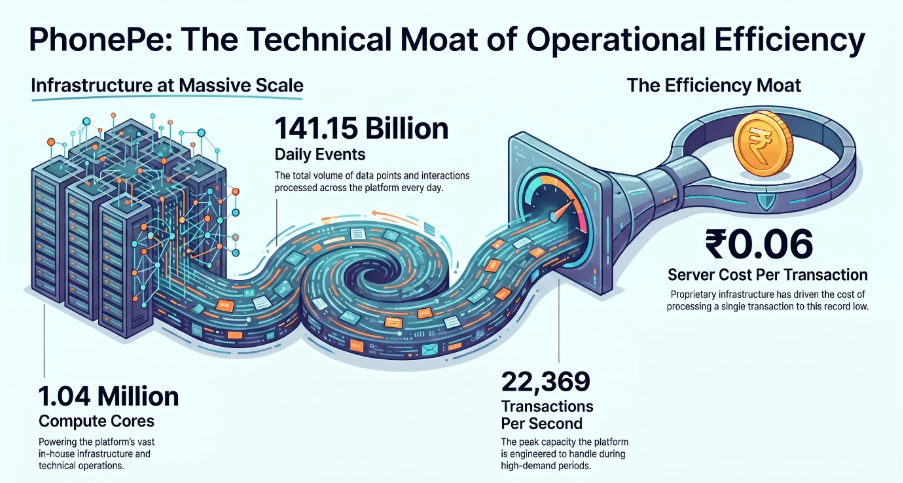

Built, not rented: PhonePe’s efficiency is engineered, not outsourced

Source: PhonePe Draft Red Herring Prospectus filed with SEBI in Jan 2026

Rather than abstracting away its technology stack through global cloud providers, PhonePe made a deliberate choice to invest in in-house, India-based data infrastructure. The result is a system optimized for local scale, evolving regulatory requirements, and cost efficiency:

- The ability to process over 141 billion events daily

- Peak throughput of tens of thousands of transactions per second

- A cost per transaction of just ₹0.06

These are not simply operational metrics-they are value appropriation mechanisms. Owning the stack translates directly into structural advantages: greater control over performance and uptime, faster innovation cycles, reduced dependency on external vendors, and stronger alignment with data sovereignty requirements.

“Investors, while appreciating past performance, are fundamentally interested in future returns. Hence, firms should strive to create future value,” says Professor Rajendra Srivastava of ISB. For PhonePe thus, in a market characterized by massive scale, thin margins, and rapidly evolving regulation, proprietary infrastructure is not just a technical detail. It is a durable source of competitive differentiation that compounds over time.

4. The Flywheel Model: From Value Creation to Value Appropriation

The long-standing critique of digital payments businesses has been a fundamental one: they scale rapidly, but struggle to monetize. Payments, at their core, are low-margin, high-volume infrastructure.

PhonePe appears to have internalized this constraint early-and structured its business accordingly. Payments were always the entry point, not the destination.

What starts as a payment ends as a financial relationship

Source: PhonePe Draft Red Herring Prospectus filed with SEBI in Jan 2026

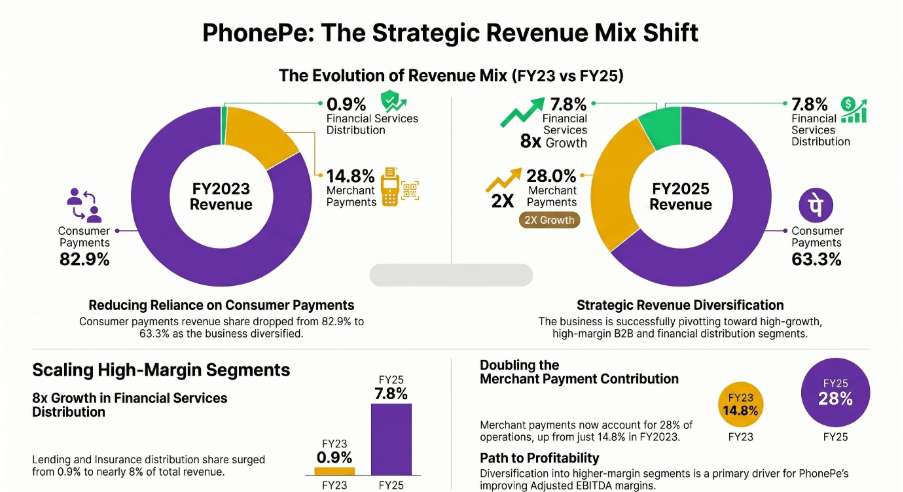

The core logic is a flywheel designed explicitly to shift from value creation to value appropriation: high-frequency transactions generate user trust, which enables cross-selling of financial services, which drives monetization.

The revenue mix now reflects this evolution, with a steady shift away from pure consumer payments toward two higher-margin streams:

- Merchant-driven revenues, reflecting the monetization of commercial relationships built at scale

- Financial services distribution-spanning lending, insurance, and wealth management-where unit economics are substantially more attractive

This is a meaningful inflection. It represents the transition from a utility platform-which creates value but struggles to appropriate it-to a revenue-generating financial ecosystem in which the value created for users becomes the basis for deepening monetization of those same relationships.

5. The Addressable Opportunity: Scope for Future Value Creation

If the first phase of PhonePe’s trajectory was about establishing behavioral and structural foundations for value creation, the next phase is about the scale of value it can generate-and appropriate-as India’s financial ecosystem matures.

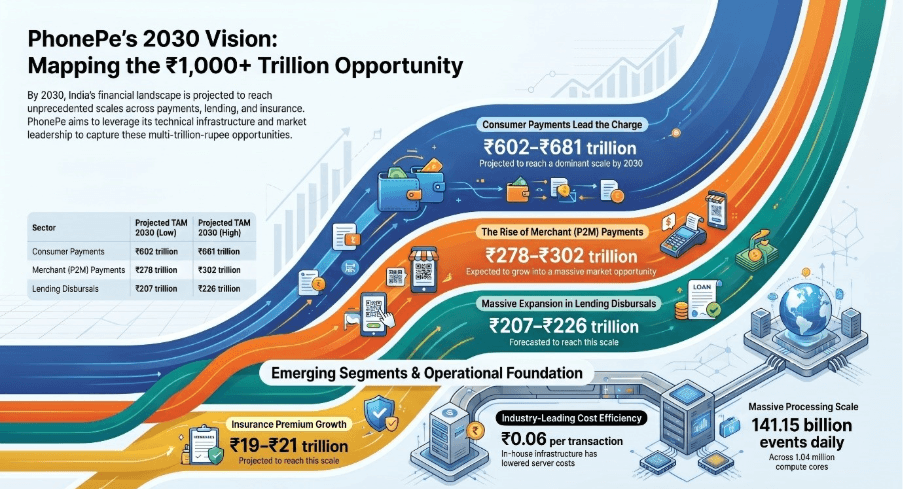

PhonePe isn’t just riding India’s growth—it’s mapping it

Source: PhonePe Draft Red Herring Prospectus filed with SEBI in Jan 2026

India’s financial ecosystem is expected to expand dramatically across consumer payments, merchant transactions, lending disbursals, and insurance penetration-a multi-trillion-rupee opportunity over the decade ahead.

What positions PhonePe to appropriate a disproportionate share of this value is not mere participation in the market, but its structural positioning within it. It already holds:

- One of the largest and most active user bases in the country

- Deep merchant penetration across urban and semi-urban markets

- High-frequency engagement that sustains top-of-mind presence

- Expanding trust across financial services categories

This means PhonePe can enter adjacent markets not as an unfamiliar challenger, but as an existing habit layer-carrying the trust and behavioral familiarity accumulated over years of high-frequency interaction. The cost of user acquisition in new verticals is therefore dramatically lower than for competitors entering fresh.

Navigating Constraints: When Appropriation Requires Recalibration

No platform operating at this scale is free of structural constraints on value appropriation.

Regulatory oversight-from the Reserve Bank of India, the Securities and Exchange Board of India, and the Insurance Regulatory and Development Authority of India-is a governing feature of the financial services landscape. The proposed UPI market share cap introduces a ceiling on further expansion of transaction dominance, limiting one traditional avenue of value appropriation.

PhonePe’s strategic response to this constraint is instructive. Rather than seeking to grow its user base further, it is redirecting its focus toward a different mode of value appropriation:

- Deepening engagement within the existing base

- Expanding the monetizable surface area per user through additional financial services

- Increasing revenue per relationship rather than number of relationships

This pivot from scale to depth is a hallmark of platform maturity-and a necessary condition for sustaining long-run value appropriation in a regulated market.

Conclusion: A Generational Platform Built on Both Sides of the Value Equation

PhonePe today resists easy categorization.

It is simultaneously a behavioral layer embedded in the daily routines of hundreds of millions of users; a merchant network with deep geographic reach; a financial services distribution engine with expanding monetization capacity; and, increasingly, a piece of digital infrastructure that underpins how value flows through India’s economy.

What makes this configuration consequential is not any single element in isolation, but the way these layers reinforce each other. The behavioral foundation enables trust. Trust enables financial services adoption. Financial services adoption generates the revenue streams through which value is appropriated. And the proprietary infrastructure ensures that this cycle compounds at a cost structure competitors find difficult to replicate.

When a platform reaches the point where millions rely on it reflexively, it has achieved something beyond product-market fit. It has become a structural feature of the system it operates within.

In India’s rapidly evolving digital economy, PhonePe is not just participating in that system-it is helping to define it. And in doing so, it has positioned itself to create and appropriate value at a scale that few platforms anywhere in the world have managed.

PhonePe filed its Draft Red Herring Prospectus with SEBI and received regulatory approval in January 2026. An official IPO date has not yet been announced. This article reflects publicly available information from PhonePe’s DRHP and market reports.

Shivani is a researcher at the Indian School of Business, Hyderabad, where she works with Professor Rajendra Srivastava on bridging academic theory with real-world business strategy. With a background as a lecturer in economics at Delhi University, she brings a strong analytical foundation to her work. Her research focuses on data-driven business solutions, examining how organizations translate strategic concepts into practice.